Image courtesy The Edge Malaysia

When it comes to retirement, it is first about setting your retirement goals. And then it is about coming up with a sound and prudent savings programme that helps you achieve those goals. In Malaysia, we are lucky to have a national social security savings system, also known as the Employees Provident Fund (EPF), to help us save for retirement, so we can sleep soundly at night.

What should retirement be about? It should be about enabling you to continue with your economically and socially productive activities and lifestyle pursuits, be it for work or leisure. Since the proportion of time you allocate to each category will change from your working years to retirement, you have to be sure of three things on the financial front so you can freely pursue your goals and activities, and meet your consumption and healthcare expenses, even while in retirement:

- That you receive a reasonable retirement payout every month.

- The payouts should last for as long as you live.

- It should preferably be indexed to the cost of living.

What could we do to help nudge our nation’s retirement savings path towards a more correct direction? Here are three basic proposals we suggest:

1. The default mode on retirement should be a version of the EPF periodical payment withdrawal scheme. This provides for a regular income stream during retirement instead of a lump sum withdrawal. The latest EPF 2021 annual report states that only 271 members are on this scheme. Down south, Singapore’s Central Provident Fund (CPF) has implemented such measures more than a decade ago with the introduction of the Retirement Sum Scheme (RSS) and later, the CPF LIFE scheme.

2. To help the B40 and M40 groups accumulate more retirement savings during their working years, the employer contribution portion needs to be increased for these groups. On the other hand, for the T20 (top 20% income group), the employer contribution amount can be capped at a certain income limit. This capped contribution to tax-advantaged retirement funds has been a feature in many countries including Singapore and the US.

3. Last but perhaps most important, form a “The Future of Malaysian Pensions Advisory Panel” comprising industry financial experts, finance academics, EPF, financially trained civil servants from the appropriate ministries and so on to review Malaysia’s pension and social security savings scheme. It can perhaps be chaired by the most knowledgeable person with reference to pensions from EPF (or co-chaired with a secretary-general from the Ministry of Finance). The panel should come up with recommendations that can be considered by the government and/or parliament for implementation. That’s what Singapore did in 2014 via its CPF Advisory Panel, where the panel made important, value-added changes to the CPF scheme, which were all implemented by 2016 (just two years later).

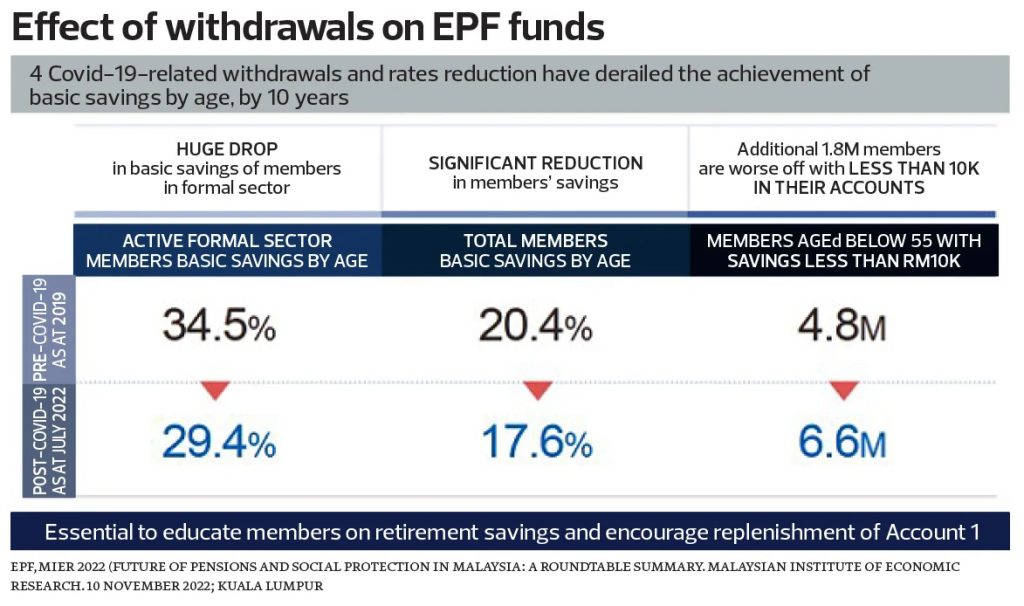

Given the dire state of inadequate EPF savings in Malaysia, with around 73% of members having too little savings by EPF’s definition, the need to set up some kind of Malaysian SuperFund to support a Basic Pension Scheme appears imminent to some experts — that is, a Basic Living Wage provision within the SuperFund that is means-tested and needs-based given that the well-to-do don’t need subsidies or government handouts.

Prof Geoffrey Williams suggested during the Policy Roundtable to use excesses from a Malaysian petroleum fund (creating one if it doesn’t exist). Just the way Norway funds its pension system via the Norges Bank (NBIM or the Government Pension Fund Global), which states, “The aim of the oil fund is to ensure responsible and long-term management of revenue from Norway’s oil and gas resources, so that this wealth benefits both current and future generations.” This is something the Malaysian pensions advisory panel can perhaps take up as part of its deliberations.

In conclusion, these principles and ideas are presented here to hopefully ensure that Much Ado About Our EPF doesn’t turn into Much Ado About Nothing (of Shakespearean proportions)!

Joseph Cherian is practice professor of finance at the Asia School of Business in Kuala Lumpur and Cornell University (visiting) in New York. Ong Shien Jin is professor of practice at the Asia School of Business and an international faculty fellow at MIT Sloan.

Originally published by The Edge Malaysia.