International financial centres (IFCs) serve as beacons for countries on the global finance stage. An IFC is like the nucleus of a nation’s financial activities, helping to connect financial zones in the country to international trade.

Growing and emerging markets have become more attractive to large global financial institutions as they provide a perfect combination of good talent, connected infrastructure, and world-class living at relatively affordable costs.

As global cities seek to ride this momentum and bolster their reputations as IFCs to attract capital, strategic insights to stand out in an increasingly competitive space become pertinent.

Metrics like the Z/Yen’s Global Financial Centres Index provide industry-trusted rankings of IFCs. But they are built on vast amounts of data and black box models that are less immediately actionable for financial centres.

IFCs should instead draw on competitive strategy theory and seek to identify and occupy what a US academic once described as “a lonely place on the frontier”.

By identifying multiple aspects that a host city or country excels in, an IFC can identify its comparative advantage, especially when combined to form a more unique proposition, and then building upon them to establish a core strategic position.

This can help the IFC to differentiate itself from competitors. Investors can then make more informed decisions about where to focus their activities based on specific value propositions and which IFC best fits their own mandates.

Case study

Malaysia illustrates how an IFC can identify comparative advantages and then exploit them.

In February 2024, the Tun Razak Exchange (TRX) in Kuala Lumpur, the Malaysian capital, was designated as the Southeast Asian country’s IFC.

Malaysia’s advantage comes from balancing conventional and Islamic practices while staying relatively neutral geopolitically and maintaining strong ties to key global regions. This can be seen from its history.

During the 1998 Asian financial crisis, Malaysia charted its own path instead of accepting aid from the International Monetary Fund. The government imposed selective capital and currency controls on outflows and established dedicated institutions to restructure distressed banks and corporations.

The unconventional approach drew scepticism from international financial institutions, which later came to see it as a pragmatic and effective policy response. It has since been widely cited as an instructive example of how developing economies can preserve financial stability, regain monetary policy autonomy, and accelerate economic recovery during periods of severe external and financial stress.

More broadly, Malaysia’s decisive response during the crisis helped cement its reputation for institutional pragmatism and financial innovation within the conventional financial system.

Malaysia has also led the way in the development of modern sukuk or Islamic bonds. Shell Malaysia, a non-Islamic corporation, issued the world’s first corporate sukuk in 1990.

The country’s Islamic financial market is not only well-developed and innovative but is also capable of attracting conventional investors who are not strictly looking for shariah-compliant financial products.

Other IFCs are more prominent in conventional finance. And some Middle Eastern cities are making increasingly ambitious moves in sukuk markets. But Kuala Lumpur is uniquely positioned to promote itself as a financial hub at the nexus of Islamic and conventional finance and attract a broader investor base seeking enhanced credit, liquidity and product diversification.

Indeed, Malaysia’s conventional and sukuk bond market is widely regarded as one of the most developed and active in Asia, estimated at US$557 billion as of November 2025.

Academic theory suggests that diversification across financial instruments with differing risk/return, structural, legal, and investor-base characteristics can provide a hedge against market volatility and systemic shocks.

Consistent with this view, during the 2008 global financial crisis, Malaysian conventional bonds experienced the widespread flight to quality effect with widening yield and repo spreads. But sukuk demonstrated relative resilience, with both yield and repo spreads reversing in its favour, reflecting differences in investor composition, risk-sharing structures and market dynamics.[1]

Malaysia’s competitive advantage is further bolstered by its ties to the rest of the world. Geopolitically, the country has remained relatively neutral, maintaining strong ties to the US, Europe, China and the rest of the Asia Pacific region, as well as the Middle East. This means it can connect multiple disparate regions and attract international capital flows, tapping into the demand for diversification.

One strategy to achieve this is to expand sukuk issuance in major global currencies such as the US dollar and the Chinese renminbi. This would reduce transaction frictions for international investors in dollar-denominated markets while positioning Malaysia to capture growing demand from renminbi-based investors and capital pools.

Kuala Lumpur can also pursue unique financial innovations that other IFCs cannot potentially offer, such as sustainable finance.

Unlike most other major Islamic hubs, Malaysia has abundant nature-based capital, including extensive rainforests, peatlands, mangrove ecosystems, and rich biodiversity assets.

Islamic finance principles have a strong conceptual alignment with environmental, social and governance, and climate finance objectives, particularly through an emphasis on asset-backing, risk-sharing, stewardship, and socially responsible investment.

This means Kuala Lumpur is uniquely positioned to develop and scale Islamic nature-based financial instruments anchored in natural capital. These may include sukuk and other shariah-compliant structures linked to conservation finance, carbon markets, biodiversity preservation, and sustainable land use.

This strategic positioning will further reinforce Kuala Lumpur’s role as a leading hub of financial innovation at the intersection of Islamic finance and sustainable finance.

Hub-and-spoke model

A country may have several financial zones with their own specialisations, functions and priorities. A financial centre differs from a financial zone in that it underpins and enables the other zones in their activities and specialisations. So IFCs and their respective zones can be treated as financial hub-and-spoke systems.

A successful financial hub must possess deep and liquid markets, supported by a well-established ecosystem of financial institutions, regulatory authorities, and complementary professional services. International investors must be able to transact efficiently within a transparent and predictable regulatory environment, complemented by strong legal infrastructure and seamless connectivity through world-class transportation and logistics networks.

These factors will allow the hub to integrate effectively with global capital markets and attract sustained international participation.

Kuala Lumpur benefits from having deep capital markets and multiple regulatory bodies such as Bank Negara Malaysia and Securities Commission Malaysia. It is also well-connected globally through international flights.

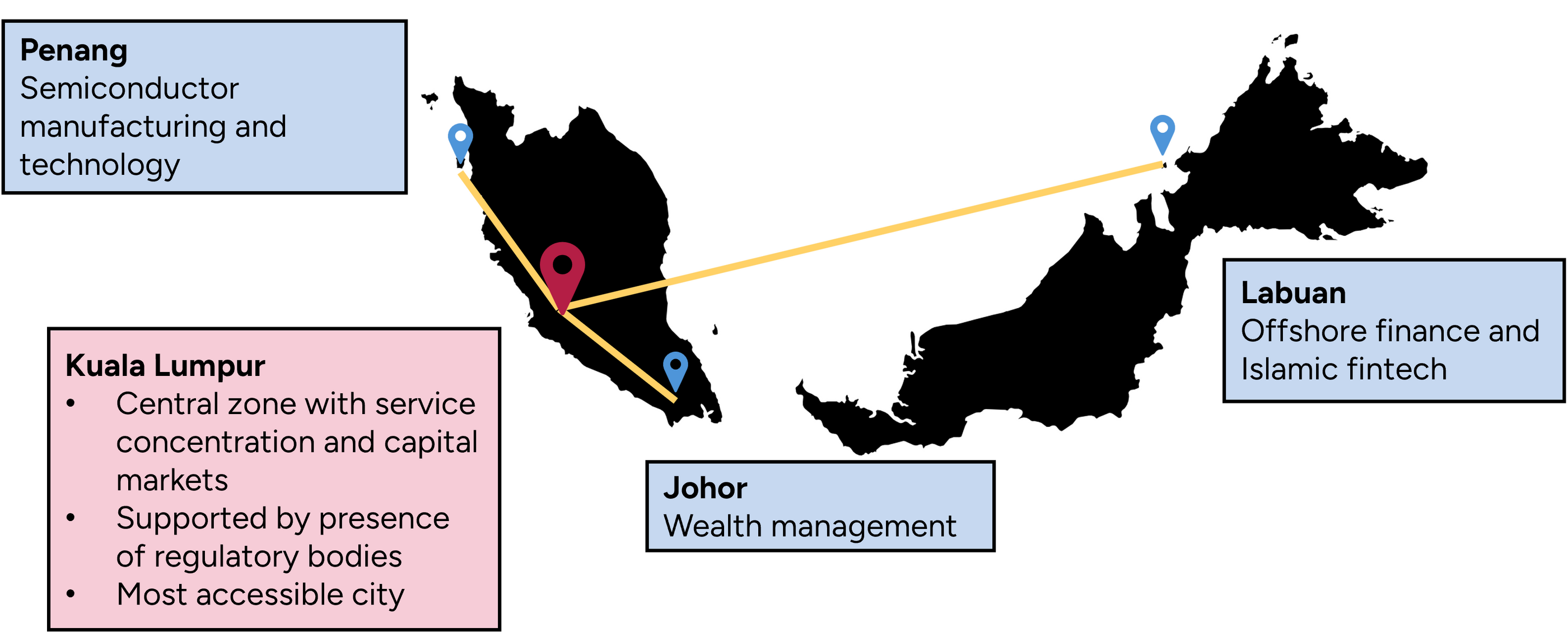

Kuala Lumpur serves as a strong hub that can be supported by other zones across the country ( Figure 1) that can act as the spokes.

Labuan, an offshore financial centre in East Malaysia that also specialises in Islamic financial technology, can lend its expertise in asset tokenisation to Kuala Lumpur while benefitting from trade through investors in the IFC.

The southern state of Johor provides wealth management and family office services, which can be further differentiated by leaning into the overall Islamic finance IFC strategy from Kuala Lumpur.

Meanwhile, the northern Penang state’s reputation in semiconductors, manufacturing and technology allows for firms in that zone and beyond that are expanding their operations to tap into Kuala Lumpur’s deeper financial market.

Figure 1. The hub-and-spoke model applied to Kuala Lumpur as a hub (red) and Labuan, Johor, and Penang and spokes (blue).

Talent strategies

An IFC’s competitive strategy should be supported by strong talent policies, including talent mobility. Relying on external talent may seem contradictory to a country’s national agenda, but it will increase the size of the talent pool so that employers can make hiring decisions that best suit their needs.

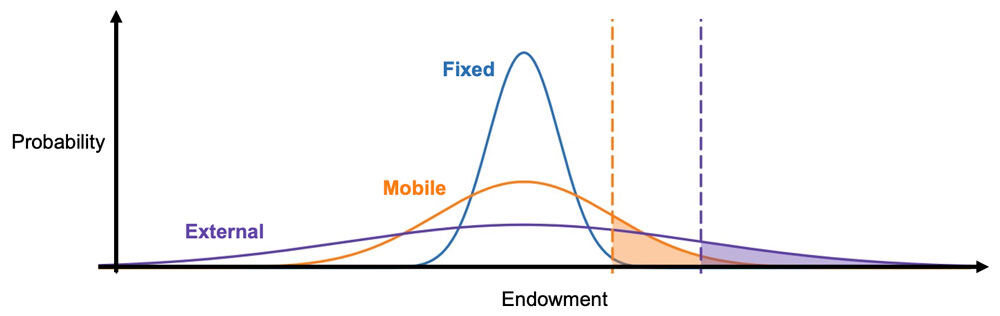

A simple financial economic model can be used to illustrate this point. We can extract talent mobility by considering the endowment distributions of fixed, mobile and external talent. Even if we assume that all three groups share the same mean endowment, each group has a different variance.

By virtue of increasing diversity and exposure, the fixed talent pool has the narrowest distribution, while the mobile and external talent pools have wider distributions, meaning that the latter pools have increased odds of finding better-performing outliers.

Employers in this model seek to make optimal hiring decisions and maximise productivity from endowment. Therefore, they hire mobile and external talent only if the talent has sufficiently high endowment such that their productivity outweighs the costs of relocating them for a new job.

Allowing employers to tap into talent pools with wider endowment distributions allows them to reach talent whose productivities outweigh their associated friction costs (Figure 2).

Figure 2. Illustrative distributions of the fixed (blue), mobile (orange), and external (purple) talent pools. Broken lines and shaded regions indicate mobile and external talent for which employers are willing to justify friction costs.

Different IFCs may adopt different strategies to facilitate talent mobility for both returning and international talent. For example, they can leverage their mandates to reduce costs for employers seeking the most appropriate talent for their needs, making it easier for employees to pursue work opportunities that are in a country’s national interest.

IFCs can also partner with the companies they host to accumulate data on hiring needs and make decisions and design policies accordingly.

The workforce at an IFC can also benefit from upskilling initiatives. As the financial and artificial intelligence sectors shift and evolve rapidly, continuous education becomes even more vital for professionals to react quickly and strategically to new trends.

To facilitate this process, an IFC can form strategic partnerships with leading academic institutions to connect companies to tailored education opportunities that can keep their talent competitive, upskilled and productive.

TRX partners Asia School of Business

In Malaysia’s case, the TRX emphasises service excellence as a core component of its talent attraction and mobility strategy. As part of this efforts, it has established a strategic partnership with the Asia School of Business to provide thought leadership, executive education, and microcredential programmes in both core and frontier areas of finance and management.

These programmes enable professionals to remain current with evolving developments in finance, leadership, supply chains and sustainability, while also strengthening capabilities in rapidly emerging technological domains such as AI and blockchain.

These initiatives enhance the broader IFC ecosystem by equipping professionals from high-value and high-growth industries with the advanced skills necessary to support innovation, competitiveness, and long-term economic growth.

Established international financial centres like London, New York, Hong Kong and Singapore have long been integral to the global financial landscape. But their comparative strengths lie primarily in conventional finance.

Emerging IFCs that are able to identify their comparative advantages and act on them will be able to effectively create and capture value, helping them to stand out globally while drawing more trade to their countries.

An IFC can extend its comparative advantage by publicising how it excels in a particular area of finance, such as through thought leadership efforts.

To be sure, not everything an IFC does needs to be completely unique. There will always be core services and transactions that investors expect from any IFC. But offering specialised, differentiated services can help investors decide whether to do business at a particular IFC.

* Lim Wei Han is an alumnus of Asia School of Business (ASB) and MIT’s School of Engineering. He is currently a research associate at Asia School of Business.

**This article draws on extensive research conducted for the TRX/Asia School of Business International Financial Centre Project and builds upon the analytical framework and findings developed in that context.

I would like to thank colleagues from Asia School of Business and MIT for their extremely helpful conversations, which shaped and strengthened this article. In particular, I am grateful to Professors Adrien Verdelhan, Asad Ata, Donald Lessard, Melati Nungsari, Pieter Stek, Renato Lima de Oliveira, Samuel Flanders, and Shardul Phadnis, whose insights helped to inform, clarify, and inspire key aspects of this research.

Originally published by Asia Asset Management.