Payments Network Malaysia Sdn Bhd (PayNet), the national payments network and a central driver of Malaysia’s digital economy, has launched what it claims is the country’s first fintech-focused community and accelerator: the PayNet Fintech Hub. In a statement, the company said this platform will accelerate fintech growth in Malaysia by providing startups with direct access to capital, key industry connections, financial incentives, and opportunities to learn from and collaborate with global leaders.

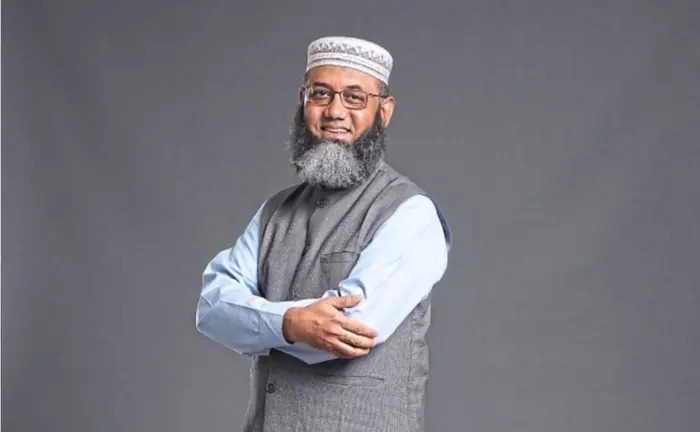

Farhan Ahmad, group CEO of PayNet, said: “A thriving fintech industry is key to delivering future-ready and inclusive financial services that can advance Malaysia’s growth and innovation goals. Successful fintech innovation is one of the best ways to ensure that Malaysia keeps pace with the fast-evolving nature of financial services, particularly due to the rapid growth of AI.”

He added that the PayNet Fintech Hub marks a decisive step forward in enabling this vision.

The Hub is a highly selective programme built around two key pillars: community and catalyst. Fintechs selected for the community will gain access to:

- A network of like-minded founders and ecosystem players for idea exchange and peer learning

- Over 450 hours of hands-on mentorship from successful founders and domain experts

- Major corporate players from banking, payments and tech for partnership opportunities

- A pool of fintech investors offering mentorship, evaluation, and potential investment

All community members will also receive exclusive financial support, including:

- More than US$238,000 (RM1 million) in PayNet value-added credits

- Over US$141,000 (RM600,000) in sponsored advisory services across legal, finance, HR and market research

- Up to US$706,000 (RM3 million) in cloud credits and support from major providers

- Access to a fully sponsored co-working space

These curated benefits are designed to help founders manage costs, overcome challenges, refine business models, sharpen go-to-market strategies, raise funds, and define clear paths to successful exits.

In addition, the most promising startups from the community will be handpicked for the exclusive Catalyst programme.

This track, developed in partnership with leading global institutions, offers top Malaysian fintechs international exposure, resources and mentorship. Participants will take part in a fully sponsored ten-week accelerator hosted by Imperial College London, one of the world’s leading startup accelerators.

The programme includes a week-long trip to London to engage with Imperial faculty, European and American startups, and culminates in a demo day that offers exposure to venture capitalists and potential corporate partners. This bespoke accelerator, designed for Malaysian fintechs, is fully funded by PayNet.

The firm also announced an expanded Fintech Hub partnership with AWS, providing Catalyst participants with credits to access AWS cloud services through the newly launched AWS Asia Pacific (Malaysia) Region. Participants will also gain entry into the upcoming Fintech Innovation Sandbox, enabling secure and scalable growth.

“The PayNet Fintech Hub is a unique and transformative initiative dedicated to scaling startups beyond the foundational stage. It directly addresses the key challenges faced by fintechs in Malaysia and is expected to significantly accelerate industry growth,” Farhan added. “The Hub is our response to the global call for smarter collaboration and accelerated innovation—uniting a fragmented ecosystem to create real, scalable outcomes. We’re very excited about its potential.”

By offering direct access to essential resources, the PayNet Fintech Hub aims to fuel innovation, foster high-impact partnerships, and position Malaysia as a leading fintech destination in the region.

For more information or to apply as a fintech startup, visit https://fintechhub.paynet.my

Originally published by Digital News Asia.